Nov 15, 2018 | Real Estate 101

You’re shopping for a new home. You drive to visit a recent listing. As you walk through the front doors, you’re impressed. Every room looks fantastic. You see yourself relaxing on the spacious patio, cooking in the modern kitchen, and enjoying evenings with the family in the cozy living room.

You’re shopping for a new home. You drive to visit a recent listing. As you walk through the front doors, you’re impressed. Every room looks fantastic. You see yourself relaxing on the spacious patio, cooking in the modern kitchen, and enjoying evenings with the family in the cozy living room.

Your emotions are on overdrive.

This is your dream home! Should you make an offer? Probably. In fact, you should make that decision quickly in case there are other interested buyers.

However, your decision shouldn’t be guided purely by emotion. You want to make sure you take practical matters into consideration too.

For example, you’ll want to consider:

- Is the property within your price range?

- Does it have everything you need?

- Do you like the neighbourhood?

- How old is the property?

- Are there items, such as the furnace, that may need to be replaced soon?

- Will it need any major repairs or upgrades?

- What are the average monthly costs of carrying the home? (Property taxes, utilities, etc.)

Once you’ve considered the purchase of the home from a practical standpoint, you’ll have a lot more confidence in your decision when you make an offer.

Need help?

Email Beth for more information

Nov 13, 2018 | Real Estate 101

When you’re having a garage sale, one of the toughest tasks is pricing your items. If you put a price tag on your old golf clubs that’s too high, no one will buy them. If you make the price too low, they might sell quickly, but you’ll spend the rest of the day wondering if you could have gotten more!

When you’re having a garage sale, one of the toughest tasks is pricing your items. If you put a price tag on your old golf clubs that’s too high, no one will buy them. If you make the price too low, they might sell quickly, but you’ll spend the rest of the day wondering if you could have gotten more!

It’s similar to selling your home — except with your home, the stakes are much higher. You want to price your property to sell, but you don’t want to leave any money on the table.

How do you accomplish that?

Setting the right list price for your home requires a combination of skilled calculation and industry savvy. Let’s start with the “calculation” part…

When you work with me, I’ll review recently sold properties that are similar to yours in type, size, features and location. Then, using that data, we’ll calculate a range that represents your property’s “current market value.”

For example, consider a spacious 15-year-old bungalow in a nice neighbourhood. If similar homes in the area have sold for $475,000-$550,000 in the last six months, then it’s obvious that your home should sell in that range too. A list price above or below that range would be in the danger zone.

But skilled calculation is only half the task.

Setting your list price also requires expertise in the local market, combined with good old-fashioned gut instinct. That instinct comes from being on the front lines of many property transactions.

That’s why working with a good real estate salesperson is so important, when you’re deciding on the list price for your home.

Want to discuss selling your home?

Contact Me

Aug 22, 2018 | Real Estate 101

If you’re shopping for a new home, you’ll likely be looking for a property that has been well cared for by it’s owners. A home that is in a good state of repair and may even be “move-in ready”, can ultimately save you time and money.

A well looked after property often has the following characteristics:

- No scuffs and dents on walls that look like they’ve been there for years.

- Major appliances are in good working order.

- Caulking around the bathroom tub or shower looks solid with no cracks, breaks or yellowing from water infiltration.

- The flooring looks clean and well-maintained. (If there is carpeting it looks like it has been regularly vacuumed.)

- Proper lighting is installed and working in all areas.

- Seals around windows look good with no sign of air infiltration.

- Exterior landscaping is well groomed.

Beside those traits, a well-maintained property will tend to make a great impression. In some cases, you’ll think, “Wow, the owner really took care of this place.” Trust that instinct. It’s probably true!

Aug 10, 2018 | Real Estate 101

Royal LePage has released it’s Boomer Property Trends Report. The release includes results from a poll conducted by Leger surveying Canadian baby boomers (currently aged 54 to 72) on real estate trends, which we believe will have a significant impact on the real estate market within the next five years.

Key highlights include:

- 17 per cent of Canadian baby boomers are planning to purchase a new home in the next five years.

- 56 per cent of boomers consider their local housing market unaffordable for retirement.

- 9 per cent of boomer parents do not expect their kids to move out until after the age of 35; this number is almost three times higher in British Columbia.

- Many boomers are willing to help their children with real estate purchases. If asked for assistance by their child, 41 per cent would give less than 25 per cent of the home’s total value, while 5 per cent would give 25 per cent of the home purchase price or higher.

- Canadian baby boomers who plan to purchase a home in the next five years are most likely to buy a detached home (45 per cent), a condominium (32 per cent), a semi-detached or town home (10 per cent) and a recreational property (5 per cent).

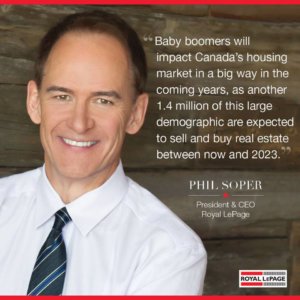

The Royal LePage Boomer Trends Survey found that 17 per cent of Canadian baby boomers (born between 1946-1964) are planning to purchase a new home in the next five years. This is expected to have a meaningful impact on the housing market, as the group represents 1.4 million[1] potential buyers and sellers. The research, conducted by Leger for Royal LePage, found that more than half (59 per cent) are opting to renovate their current residence rather than buying a new home.

The Royal LePage Boomer Trends Survey found that 17 per cent of Canadian baby boomers (born between 1946-1964) are planning to purchase a new home in the next five years. This is expected to have a meaningful impact on the housing market, as the group represents 1.4 million[1] potential buyers and sellers. The research, conducted by Leger for Royal LePage, found that more than half (59 per cent) are opting to renovate their current residence rather than buying a new home.

“Don’t count them out yet – baby boomers will impact Canada’s housing market in a big way in the coming years, as another 1.4 million of this large demographic are expected to sell and buy real estate between now and 2023,” said Phil Soper, president and CEO, Royal LePage. “While the wave of older consumers will increase competition for condominium property in particular, there is no single type of home that boomers will be investing in.”

“Our research does indicate that smaller cities and recreational areas will attract more investment than major cities,” continued Soper. “This large segment of the population views our big cities as generally unaffordable for retirement purposes.”

The survey found that 44 per cent of respondents across Canada who still have children living at home expect them to move out between the ages of 21 and 25, and 21 per cent expect them to leave between the ages 26 and 30. Eighteen per cent anticipate their children will move out after the age of 30, with 9 per cent expecting them to depart after the age of 35. This percentage nearly triples in British Columbia, where 24 per cent of respondents with children living at home expect their children to move out after the age of 35. According to Royal LePage’s Peak Millennial Survey[2] conducted last year, 14 per cent of Peak Millennials surveyed are living with their parents.

“Our 2017 research into the largest group of first time home buyers in Canada, which we call the Peak Millennials, showed many were roosting in the family nest well beyond the traditional age of exit,” Soper said. “With this work, we have confirmed that boomers are allowing children to reside at home well into adulthood. Yet they won’t stay forever, and when they go, the folks are going condo shopping.”

Retirement Plans and Perceptions on Housing Affordability

When asked about plans nearing or during retirement, one in five (20 per cent) boomers intend on buying a new property, while 71 per cent do not plan on buying a new home. Respondent sentiments were mixed on the desire to downsize, with less than half (41 per cent) stating that they would seek a smaller dwelling in retirement, while just over half (52 per cent) have no intention of downsizing.

When asked about plans nearing or during retirement, one in five (20 per cent) boomers intend on buying a new property, while 71 per cent do not plan on buying a new home. Respondent sentiments were mixed on the desire to downsize, with less than half (41 per cent) stating that they would seek a smaller dwelling in retirement, while just over half (52 per cent) have no intention of downsizing.

Considering recent home price increases in several Canadian markets, more than half (56 per cent) of boomers polled said they consider the housing market in their city or region to be unaffordable. This number jumps to 78 per cent and 63 per cent of respondents in British Columbia and Ontario, respectively. When asked about their willingness to relocate, over one-third (34 per cent) of respondents nationally stated that they are open to moving to another city or suburb where property prices are more affordable.

Financial Status and Support for Children

Overall, a large segment of the boomer population is on strong financial footing and on a clear path to being mortgage-free, if not already. According to the survey, over three-quarters (77 per cent) of those who own a home have paid off over 50 per cent of their mortgage, and 61 per cent have paid off over 90 per cent.

Overall, a large segment of the boomer population is on strong financial footing and on a clear path to being mortgage-free, if not already. According to the survey, over three-quarters (77 per cent) of those who own a home have paid off over 50 per cent of their mortgage, and 61 per cent have paid off over 90 per cent.

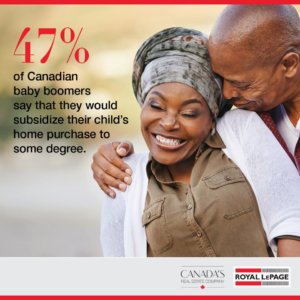

Many boomers are willing to help their children with real estate purchases, with 47 per cent affirming that they would subsidize their child’s home acquisition to some degree.

“Baby boomers are the most affluent generation in Canadian history, yet the journey has not been without challenge and adversity. Through several difficult economic recessions, the equity in their homes has proven to be wealth bedrock. This is a generation that deeply values home ownership and very much wants their children to have the same opportunity,” concluded Soper.

Summaries and Trends Specific to British Columbia

With so many boomers relying on their homes to fund their retirement, 43 per cent said they are planning to eventually downsize their principal residence and almost half (42 per cent) would consider purchasing a condominium for their next home. Thirty-seven per cent would be willing to move to a new area in search of affordability.

With so many boomers relying on their homes to fund their retirement, 43 per cent said they are planning to eventually downsize their principal residence and almost half (42 per cent) would consider purchasing a condominium for their next home. Thirty-seven per cent would be willing to move to a new area in search of affordability.

“More and more we’re seeing baby boomers in British Columbia downsizing from a detached home to a condominium,” said Michael Trites, managing broker, Royal LePage Northstar Realty. “Increasingly they are transitioning into condos to unlock some of the equity they have built up in their homes, while gaining more flexibility as their health and lifestyle preferences change.”

A vast majority (88 per cent) of boomers in B.C. believe that real estate is a good investment, and 42 per cent of respondents with children stated that they would be willing to subsidize their purchase of a home.

Home to some of the most expensive markets in the county, only 19 per cent of boomers in B.C. consider the housing market in their region affordable – the lowest rate in the county.

Click here to view the full report

Jun 26, 2018 | Real Estate 101

You don’t want to waste time looking at properties that are beyond your price range. At the same time, you don’t want to purchase a less-than-ideal home, only to realize later on that you could have afforded more.

You don’t want to waste time looking at properties that are beyond your price range. At the same time, you don’t want to purchase a less-than-ideal home, only to realize later on that you could have afforded more.

So how do you determine what type of new home you are qualified to purchase?

The first step is to find out what your current property would likely sell for in today’s market. I make that calculation for clients all the time. It involves reviewing what homes similar to yours have sold for recently, as well as other data — such as special features your home may have that are likely to boost the selling price.

Once you know the current market value of your home, subtract any outstanding mortgages and estimated selling expenses, and you’ll end up with an amount that can be applied to the purchase of your next home. (You may also have other funds you want to use.)

The next step is to talk to a lender or mortgage broker to see how much of a new mortgage you qualify for. (Call me if you need a recommendation.) It’s important to get a Pre-Qualification or Pre-Approval. That makes the offer you make on a new home more credible.

If you want to find out the types and sizes of homes you can get into, give me a call. I’d be happy to show you the possibilities!

Contact Beth

May 30, 2018 | Real Estate 101

Buying a new pair of shoes is relatively easy. Once you find the style you like, all you need to do is try them on and see if they fit. If they do, you go to the cash register and pay.

Buying a new pair of shoes is relatively easy. Once you find the style you like, all you need to do is try them on and see if they fit. If they do, you go to the cash register and pay.

When it comes to size, buying a new home can be trickier! Whether your intention is to upsize or downsize, figuring out the right size can be especially challenging.

Say for example, you’re downsizing from a large two-story home to a smaller bungalow. You don’t want to underestimate the space you need and end up in a place that feels tight. If you’re going the other way and upsizing, you don’t want to end up sinking extra money into a property that’s larger than you really need.

So how do you avoid these scenarios?

One of the best ways is to start by considering your current home. Do you use all the rooms in your home regularly? Is there a bedroom that’s rarely occupied? Has the recreation room become simply a storage area? If you’re downsizing, subtracting rooms your scarcely use can give you a better idea of what you need in a new home.

Upsizing is a bit more challenging because you have to anticipate what you will need in the future. For example, if you have young children and your place is feeling cramped, then a home with a recreation room or separate family room and living rooms may be a good idea. You may also need a bigger kitchen with a spacious eating area (in addition to a separate dining room). Think about the extra room you’ll need and how you’ll use that space.

When I work with a client, I typically sit down with them and discuss the type of home they want, in detail – and, based on needs and circumstances, I make expert recommendations. Bottom line, I help clients find the perfect fit in a new home.

Contact me if you'd like to learn more